- Product

- Spend Management

- Accounts Payable

- Team & Field

- Platform

- Industries

- Clyr VS

- Partners

- Blog

- Contact Us

- Login

Get Free Demo

How Clyr compares with Brex for companies that run on job sites rather than venture funding.

| Feature | Brex | |

|---|---|---|

| Works with the cards and bank accounts you already have | ||

| No credit application or underwriting required | ||

| Serves Main Street businesses, not just startups and enterprises | ||

| Accounts Payable automation | ||

| Employee reimbursement | ||

| Receipt capture via SMS, email, or browser with no-login links | ||

| Two-way sync with AppFolio, Buildium, ServiceTitan, Jobber, and more | ||

| Job costing and billable expense markup | ||

| Utility bill management | ||

| 1099 e-filing built in | ||

| Compliance leaderboard for receipt follow-ups | ||

| Built for property management, construction, and field service | ||

| 24/7 US-based support via phone, SMS, and email |

“The real-time transaction notifications and AI-based coding have streamlined our processes, and the absence of a proprietary card means we maintain our banking relationships. Plus, the ongoing US-based support is a game-changer for our nationwide teams.”

Brex built a powerful spend platform around its charge card: corporate cards, banking-style accounts, travel booking, and AI-assisted expense automation. In April 2026 the company officially became part of Capital One. Clyr plays a different game entirely: card-agnostic expense automation for property managers, contractors, and service companies, with receipts by text and coding to jobs and properties.

Brex has always been explicit about its market. In 2022 it famously offboarded tens of thousands of small traditional businesses to focus on venture-backed startups and enterprises, and its underwriting still reflects that focus. Add the card requirement (the platform's economics run on Brex card spend) and the 2026 Capital One integration, whose long-term effect on product and policies is still unfolding, and many small and mid-sized operators conclude the platform simply is not aimed at them.

Brex under Capital One will likely gain resources, but acquisitions of this size reshape roadmaps, risk policies, and account criteria in ways buyers cannot predict from outside. If your business was already at the edge of Brex's underwriting appetite, that uncertainty is worth weighing. Clyr carries none of it: no credit relationship, no underwriting, and no dependency on a card issuer's strategy, because your existing cards stay exactly where they are.

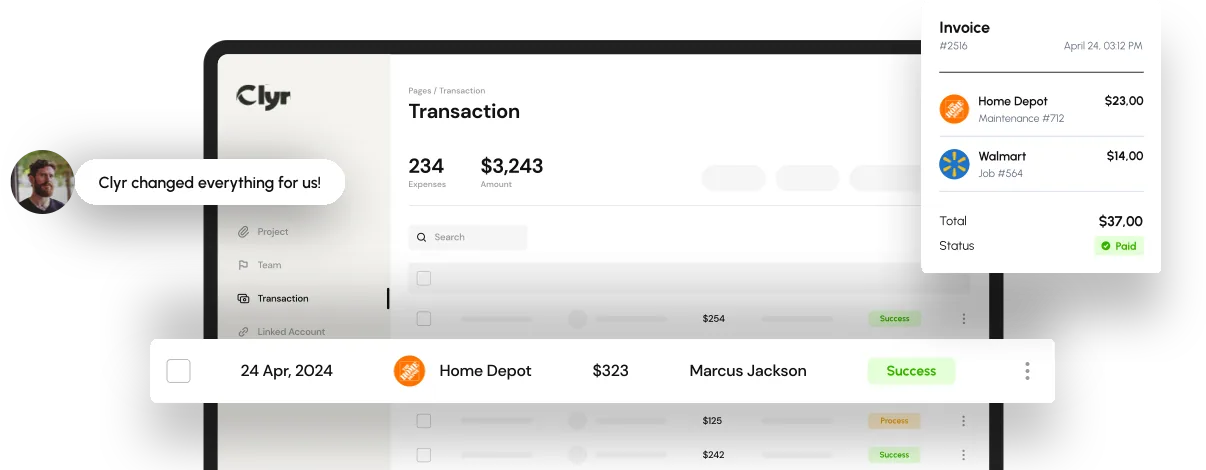

Brex automates spend on Brex cards elegantly: policies, limits, and AI-assisted review. Clyr delivers that class of automation across every card you already have. A swipe on any connected card triggers a real-time text, the employee replies with a receipt photo, and AI coding rules assign vendor, category, class, and job. Clyr then covers ground Brex does not: billable expenses with markup, utility bill management, vendor management with 1099 e-filing, and job costing designed for crews, not cap tables.

Brex integrates with the systems startups run: accounting suites, HRIS, travel. Clyr syncs two ways with QuickBooks, NetSuite, Xero, and Sage, and then with the operational platforms field businesses live in: AppFolio, Buildium, Rent Manager, RentVine, Jobber, ServiceTitan, Service Fusion, Hostaway, and 25+ in total, so every expense lands on the right property, unit, or job. See the integrations page.

Brex vs Ramp is a fair fight between two card-first platforms funded by their own card programs (our Ramp vs Brex breakdown and Clyr vs Ramp comparison cover that model). Both assume your spend moves to their card and your company fits their underwriting. Clyr assumes neither, which is exactly why field-heavy businesses pick it.

Connect the cards you plan to keep using, export your Brex history for the archive, and map your GL, entities, and jobs during 1:1 white-glove onboarding. Teams typically go live in under a day, and employees need nothing more than their phone number to start.

If you are a funded startup that wants a charge card, banking, and travel in one place, Brex under Capital One remains a strong platform. If you are a real-world operator who wants expense automation on existing cards and job-level visibility, Clyr is the better alternative. Book a free demo and compare on your own spend.

Yes, especially for small and mid-sized field businesses. Clyr automates receipt capture, coding, approvals, and AP on the cards you already have, with no underwriting and no card switch.

Brex is a charge-card platform funded by spend on Brex cards, aimed at startups and enterprises and now owned by Capital One. Clyr is card-agnostic software built for property management, construction, and field service teams.

Capital One completed its acquisition of Brex on April 7, 2026. Brex continues to operate as a platform within Capital One.

No. Clyr is not a card or credit product. It connects to your existing cards and bank accounts, so there is no underwriting, no credit application, and no change to your banking.

Yes. In 2022 Brex offboarded tens of thousands of small traditional businesses to concentrate on venture-backed startups and enterprise customers, which is why many SMBs look for alternatives designed for them.

That is Clyr’s home turf. Job costing, billable markup, and two-way sync with AppFolio, Buildium, Jobber, ServiceTitan, and 25+ platforms are core features rather than afterthoughts.